About the Conveyance or Transfer

Note: The ‘About the Conveyance or Transfer’ section and associated questions below appear if you have selected the ‘Conveyance or transfer’ option for the ‘Description of transaction’ question in ‘About the Transaction’.

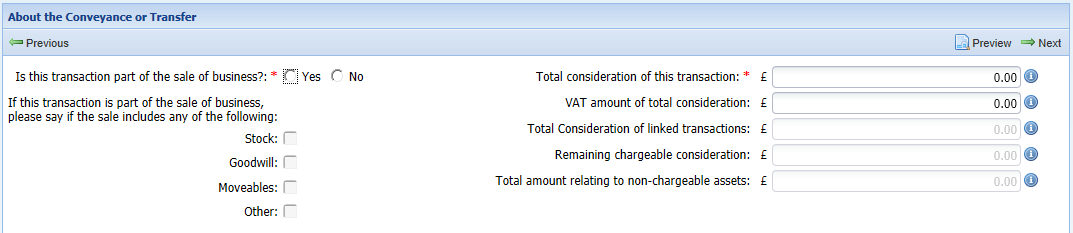

Is the transaction part of the sale of business?

You must answer this question.

Select ‘Yes’ if the transaction is part of the sale of a business (or of a part of a business) by which an interest in land (for example, land and buildings) is transferred together with other assets that are not chargeable to LBTT.

Note: If you answer ‘Yes’ then you must answer the question below as well as the later ‘Remaining chargeable consideration’ and ‘Total amount relating to non-chargeable assets’ questions.

If this transaction is part of the sale of business, please say if the sale includes any of the following

You must answer this question if you answered ‘Yes’ to the preceding ‘Is the transaction part of the sale of business?’ question. If you answered ‘No’ to that question then the options below will be greyed out.

Select as many as of the four options below which are relevant to the sale of business:

- Stock;

- Goodwill;

- Moveables;

- Other.

Note: The sum total of the above four categories needs to be entered in the ‘Total amount relating to non-chargeable assets’ question.

Total consideration of this transaction

You must answer this question.

Enter the total chargeable consideration for the land transaction, including any VAT payable.

If some or all of the consideration is uncertain or unascertained because it depends on uncertain future events, then a just and reasonable estimate of the amount of consideration should be provided. This should be determined on the assumption that the uncertain consideration will be payable.

If some or all of the consideration is contingent on an uncertain future event, then a reasonable estimate of the amount of consideration should be provided. This should be determined on the assumption that the contingency will be resolved so that the contingent consideration will be payable or, as the case may be, will not cease to be payable.

If some or all of the consideration was uncertain, contingent or unascertained and you are submitting an lbtt return (under section 31 of the LBTT(S)A 2013) because more tax has become due as a result of the contingency ceasing or the consideration becoming certain or ascertained (whichever applies), you should enter the total chargeable consideration for the transaction, including any part or parts already paid.

Chargeable consideration can consist of the payment of money and/or non-monetary method of payment (such as provision of goods and services, the assumption of financial liabilities etc.).

In some circumstances the total consideration will have to be apportioned on a just and reasonable basis in order to determine the chargeable consideration for a land transaction.

These circumstances include consideration which is attributable:

- to two or more land transactions;

- in part to a land transaction and in part to another matter; or

- in part to matters making it chargeable consideration and in part to other matters.

For further guidance on what is and is not chargeable consideration see LBTT2001 and LBTT2009 respectively.

VAT amount of total consideration

If the amount you entered against the ‘Total consideration of this transaction’ question includes VAT, enter the amount of VAT included.

Total Consideration of linked transactions

You must answer this question if you answered ‘Yes’ to the earlier ‘Is this transaction linked to any others?’ question in the ‘About the Transaction’ section.

If this land transaction forms part of a linked transaction then enter the total consideration (or value in money or money’s worth) of all the linked transactions, including any VAT (see LBTT2008).

Remaining chargeable consideration

You must answer this question if you answered ‘Yes’ to the earlier ‘Is the transaction part of the sale of business?’ question.

Enter the ‘Total consideration of this transaction’ amount less the amount apportioned to the non-chargeable assets (the figure you enter in the question below).

Total amount relating to non-chargeable assets

You must answer this question if you answered ‘Yes’ to the earlier ‘Is the transaction part of the sale of business?’ question.

Enter the total amount of consideration apportioned to the non-chargeable assets.