Scottish Landfill Tax (SLfT) is a tax on the disposal of waste to a landfill in Scotland, whether or not to an authorised landfill site. SLfT applies to all taxable disposals made in Scotland on or after 1 April 2015.

SLfT also applies to the prescribed landfill activities relating to the use of material on site that are listed in the Scottish Landfill Tax (Prescribed Landfill Site Activities) Order 2014.

http://www.legislation.gov.uk/ssi/2014/367/made

For more information about SLfT, please see the relevant sections on our website.

https://www.revenue.scot/scottish-landfill-tax

The current rates for SLfT are set by the Scottish Government and approved by the Scottish Parliament.

Table 12: Declared taxable disposals by SLfT rate and year

| Year | Declared taxable disposals (tonnes) | ||

| Standard rate | Lower rate | All | |

| 2015/16 | 1,869,300 | 1,050,300 | 2,919,600 |

| 2016/17 | 1,816,400 | 771,600 | 2,588,000 |

| 2017/18 | 1,775,100 | 790,200 | 2,565,300 |

| 2018/19 | 1,650,100 | 739,500 | 2,389,600 |

| 2019/20 | 1,343,600 | 685,700 | 2,029,400 |

| 2020/21 | 1,170,200 | 618,800 | 1,789,100 |

Standard rate disposals of 1.17 million tonnes were declared in 2020/21, a decrease of 13 per cent on the previous year, and a continuation of the long-term trend of gradually declining disposals.

During April to June 2020, standard rate disposals were 41 per cent lower than the same period of the 2019, significantly faster than the long-term trend of reducing tonnages, due to disruption resulting from the COVID-19 pandemic and restrictions. However, higher disposals in the following three quarters of the year compensated to some extent for this decrease.

Lower rate disposals of 0.62 million tonnes were declared in 2020/21. Since 2015/16 lower rate disposals have decreased by approximately 0.43 million tonnes (41 per cent). Much of this decrease in lower rate disposals occurred between 2015/16 and 2016/17, following the cessation of taxable activity by a small number of operators.

Table 13: SLfT declared due, contributions to the Scottish Landfill Communities Fund (SLCF) and credits claimed by year

| Year | £ Millions | |||||||

| Gross SLfT declared due | Contributions to SLCF | Credit claimed for | Net SLfT declared due | |||||

| Standard rate disposals | Lower rate disposals | All | Contributions to SLCF | Other | All | |||

| 2015/16 | 154.4 | 2.7 | 157.7 | 9.1 | 8.2 | 0.2 | 8.4 | 149.3 |

| 2016/17 | 153.3 | 2.0 | 156.3 | 8.9 | 8.0 | 0.3 | 8.3 | 148.0 |

| 2017/18 | 152.8 | 2.1 | 155.0 | 9.0 | 8.1 | 0.3 | 8.4 | 146.6 |

| 2018/19 | 146.8 | 2.1 | 148.9 | 8.0 | 7.2 | 0.4 | 7.6 | 141.3 |

| 2019/20 | 122.7 | 2.0 | 124.7 | 6.3 | 5.7 | 0.5 | 6.2 | 118.6 |

| 2020/21 | 110.2 | 1.9 | 112.0 | 5.2 | 4.9 | 0.9 | 5.8 |

108.3 |

Notes:

1. For 2015/16 and 2016/17 this column will not equal the sum of the previous two columns. This is because of a small number of operators who have not reported the tonnages associated with taxable disposals subject to a partial water discount. The disposals were included in the gross SLfT declared due and, therefore, do not have any tax implications.

2. Taxpayers can claim a credit equal to 90 percent of their contribution to the SLCF.

3. Credit claimed for bad debt and permanent removals

The net SLfT declared due is mainly dependent on standard rate disposals, lower rate disposals and contributions to the SLCF16 . The rates at which standard and lower rate disposals are taxed are set by the Scottish Government and vary each year. For further information on SLfT rates see the guidance published by Revenue Scotland.17

Since 2015/16 the tax rate for standard rate disposals has been around 32 times higher than that for lower rate disposals. Gross SLfT liabilities are therefore dominated by standard rate disposals.

Net SLfT declared due was £106 million in 2020/21, a decrease of £12 million (10 per cent) on the previous year. Similar to standard rate disposal tonnages, the largest decrease in revenue (and contributions to the SLCF) occurred between 2018/19 and 2019/20. The longterm decrease in net SLfT is predominantly due to standard rate disposal tonnages decreasing faster than the standard rate of tax has increased with inflation.

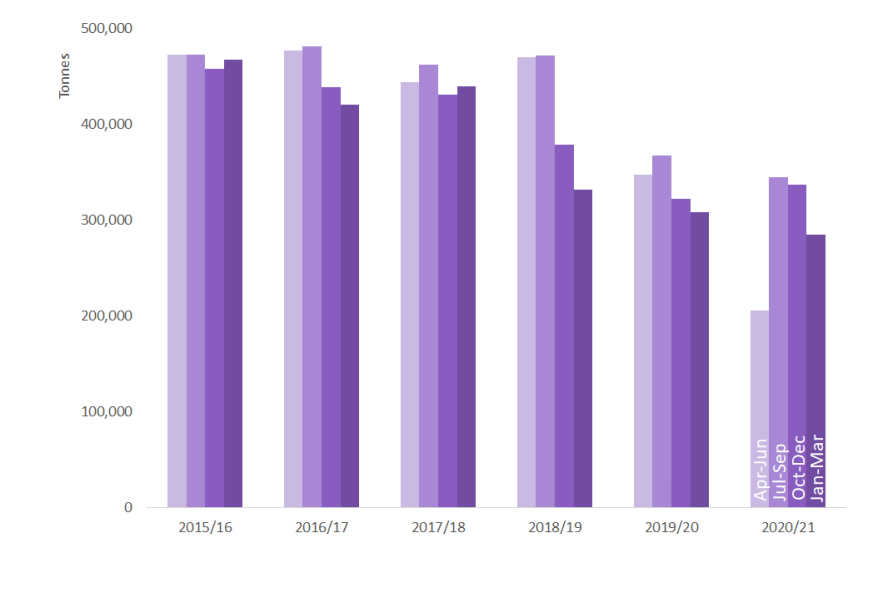

Figure 27: Declared standard rate disposals by quarter

Figure 28: SLfT declared due by quarter

Figure 27 shows declared standard rate disposal tonnages by quarter and year and Figure 28 shows the (net) SLfT declared due by quarter and year. Figure 27 shows that the standard rate disposal tonnages declared in April to June and July to September tend to be slightly higher than in October to December and January to March. April to June 2020 provided an exception to this trend as waste disposals were disrupted by impacts of the COVID-19 pandemic.

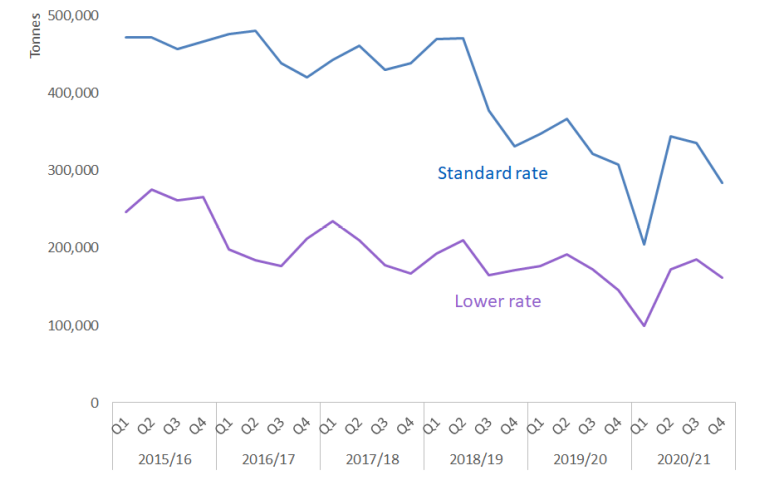

Figure 29: Declared taxable disposals by SLfT rate and quarter

Figure 29 shows declared taxable disposals by SLfT rate and quarter. In addition to the seasonality discussed above, Figure 29 shows a gradual downward trend in standard and lower rate disposals up to and including 2018/19-Q2, followed by a more marked decrease in the level of standard rate disposals from 2018/19-Q3 onwards. A clear dip is seen in Q1 2020/21 and this is likely to reflect the impact of COVID restrictions.

Revenue Scotland collects information on the types of waste constituting the taxable disposals in the supplementary spreadsheets submitted with SLfT returns. The waste is categorised using European Waste Catalogue (EWC) codes. For further information on EWC codes see the guidance published by the Scottish Environment Protection Agency.

https://www.sepa.org.uk/media/163421/ewc_guidance.pdf

Table 14: Proportion of gross SLfT declared due by EWC code and year

| EWC code | Description | Estimated proportion of total gross SLfT declared due | |||||

| 2015/16 | 2016/17 | 2017/18 | 2018/19 | 2019/20 | 2020/21 | ||

| 20 03 01 | Mixed municipal | 64.7% | 62.8% | 63.0% | 58.6% | 46.3% | 52.0% |

| 19 12 12 | Other wastes (including mixtures of materials) from mechanical treatment of wastes other than those mentioned in 19 12 11 | 22.6% | 24.0% | 25.2% | 28.7% | 35.3% | 34.2% |

| Other or unknown | 12.7% | 13.2% | 11.8% | 12.7% | 18.4% | 13.8% |

Mixed municipal waste (EWC code 20 03 01) is consistently the most prevalent waste type, contributing around 63 per cent of SLfT revenue from 2015/16 to 2017/18, falling to around 49 per cent in 2019/20 to 2020/21. A further 23 to 35 per cent of the gross SLfT due is attributable to disposals of EWC code 19 12 12 – other wastes (including mixtures of materials) from mechanical treatment of wastes other than those mentioned in 19 12 11. Disposals of these two waste streams have accounted for the majority (82 to 88 per cent) of gross SLfT declared due each year.

Note that as EWC code 19 12 12 constitutes waste “from the mechanical treatment of waste” then it will contain other waste types (i.e. other EWC codes) that have then been mechanically treated.

Table 15: Taxable disposals by EWC code and SLfT rate, 2015/16 – 2020/21

| EWC code | Description | Row percentage | Taxable disposals (tonnes) | |

| Standard rate | Lower rate | |||

| 20 03 01 | mixed municipal waste | 100.0% | 0.0% | 5,921,400 |

| 19 12 12 | other wastes (including mixtures of materials) from mechanical treatment of wastes other than those mentioned in 19 12 11 | 69.4% | 30.6% | 3,708,700 |

| Other or Unknown | 24.4% | 75.6% | 4,650,900 |

Mixed municipal waste (EWC code 20 03 01) has accounted for 5.9 million tonnes of taxable disposals over the first six years of SLfT, all of which was declared as subject to the standard rate of SLfT. EWC code 19 12 12 has accounted for 3.7 million tonnes over six years. Taxable disposals of EWC code 19 12 12 are split between the standard and lower rates of SLfT. Table 15 shows that 69 per cent of disposals of EWC code 19 12 12 where tax was declared due have been declared as subject to the standard rate of SLfT and the remaining 31 per cent have been declared as subject to the lower rate.

Further information on determining the amount of SLfT tax payable (e.g. higher or lower rate) is contained in guidance published by Revenue Scotland.

16 Taxpayers can claim a credit of 90 per cent of their contribution to the SLCF which is then deducted from their gross SLfT liability.

17 https://www.revenue.scot/scottish-landfill-tax/guidance/slft-legislation-guidance/determining-tax/slft2002