Scottish Landfill Tax (SLfT) is a tax on the disposal of waste to a landfill in Scotland, whether to an authorised landfill site or not. SLfT applies to all taxable disposals made in Scotland on or after 1 April 2015.

Table 12: Declared taxable disposals by SLfT rate and year

| Declared taxable disposals (tonnes) | |||

| Year | Standard rate | Lower rate | All |

|

2017/18 |

1,775,100 |

790,200 |

2,565,300 |

|

2018/19 |

1,650,100 |

739,500 |

2,389,600 |

|

2019/20 |

1,343,600 |

685,700 |

2,029,400 |

|

2020/21 |

1,170,200 |

618,800 |

1,789,100 |

|

2021/22 |

1,348,600 |

680,100 |

2,028,700 |

Standard rate disposals of 1.35 million tonnes were declared in 2021/22, an increase of 15% on the previous year. Lower rate disposals also increased by 10%. This marks a departure from the long term trend of decreasing tonnage year on year, due in part to facilities returning to normal disposal activities after the previous year was affected by the COVID-19 pandemic.

Table 13: SLfT declared due, contributions to the Scottish Landfill Communities Fund (SLCF) and credits claimed by year

| Year | £Millions | |||||||

| Gross SLfT due | Contributions to SLCF | Credit claimed for | Net SLfT declared due | |||||

| Standard rate disposals | Lower rate disposals | All | Contributions to SLCF | Other | All | |||

| 2017/18 | 152.8 | 2.1 | 155.0 | 9.0 | 8.1 | 0.3 | 8.4 | 146.6 |

| 2018/19 | 146.8 | 2.1 | 148.9 | 8.0 | 7.2 | 0.4 | 7.6 | 141.3 |

| 2019/20 | 122.7 | 2.0 | 124.7 | 6.3 | 5.7 | 0.5 | 6.2 | 118.6 |

| 2020/21 | 110.2 | 1.9 | 112.0 | 5.2 | 4.9 | 0.9 | 5.8 | 106.3 |

| 2021/22 | 130.4 | 2.1 | 132.5 | 6.3 | 5.7 | 1.7 | 7.4 | 125.2 |

1.Taxpayers can claim a credit equal to 90 percent of their contribution to the SLCF

2. Credit claimed for bad debt and permanent removals

Net SLfT declared due was £125 million in 2021/22, an 18% increase on the previous year. The long-term decrease in net SLfT before 2021/22 is mainly due to standard rate disposal tonnages decreasing faster than the standard rate of tax has increased.

Standard rate disposals account for the vast majority of SLfT due. Though typically the tonnages are only about twice as high as lower rate disposals, the tax rate is around 32 times higher.

Net SLfT declared due is mainly dependent on standard rate disposals, lower rate disposals and contributions to the Scottish Landfill Communities Fund (SLCF). The SLCF is a tax credit scheme for SLfT which allows landfill site operators to contribute tax credits to benefit community and environmental projects.

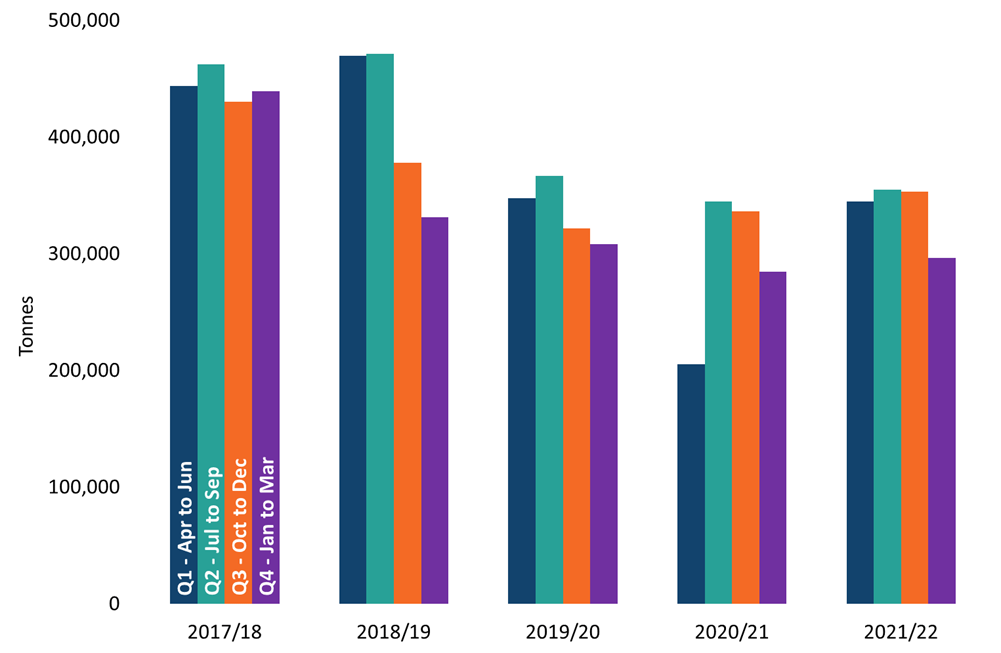

Figure 20: Declared standard rate disposals by quarter

Standard rate disposal tonnages were highest in Q1 and Q2 each year up until 2020/21. In Q1 of 2020/21, the effect of the first COVID-19 lockdown can be seen in a greatly reduced tonnage declared. In 2021/22, the tonnages declared were fairly evenly spread in the first 3 quarters of the financial year. Year on year there had been a gradual decrease in total tonnage (standard plus lower rate) until 2021/22, which has increased slightly, close to 2019/20 levels.

Table 14: Proportion of gross SLfT declared due by EWC code and year

| EWC Code | Description | Estimated proportion of total gross SLfT declared due | ||||

| 2017/18 | 2018/19 | 2019/20 | 2020/21 | 2021/22 | ||

| 20 03 01 | Mixed municipal waste | 63.0% | 58.6% | 46.3% | 52.0% | 46.1% |

| 19 12 12 | Other wastes (including mixtures of materials) from mechanical treatment of wastes other than those mentioned in 19 12 11 | 25.2% | 28.7% | 35.3% | 34.2% | 39.5% |

| Other or unknown | 11.8% | 12.7% | 18.4% | 13.8% | 14.4% | |

European Waste Catalogue (EWC) codes are a coding system used to describe and categorise waste. Mixed municipal waste the most prevalent waste type, contributing around 46% of SLfT revenue in 2021/22. A further 40% was attributable to disposals of EWC code 19 12 12 – other wastes. Disposals of these two waste streams have accounted for the majority of gross SLfT declared due each year.

Note that as EWC code 19 12 12 constitutes waste “from the mechanical treatment of waste” it will contain other waste types (other EWC codes) that have then been mechanically treated.

Table 15: Taxable disposals by EWC code and SLfT rate, 2015/16 – 2021/22

| EWC code | Description | Row percentages | Tax disposals (tonnes) | |

| Standard rate | Lower rate | |||

| 20 03 01 | Mixed municipal waste | 100% | 0.0% | 6,716,300 |

| 19 12 12 | Other wastes (including mixtures of materials) from mechanical treatment of wastes other than those mentioned in 19 12 11 | 69.1% | 30.9% | 4,290,100 |

| Other or unknown | 25% | 75.0% | 5,303,300 | |

Mixed municipal waste has accounted for 6.7 million tonnes of taxable disposals since 2015/16, all of which was subject to the standard rate of SLfT. EWC code 19 12 12 has accounted for 4.3 million tonnes over the same time span. 69% of EWC code 19 12 12 disposals were subject to standard rate tax and 31% were subject to the lower rate.