Annex D: Key Terms

| Term | Definition |

|---|---|

| Consumer duty | A requirement for public bodies to consider how their policies and services affect consumers and ensure they are treated fairly. |

| Continuous improvement (CIMP) | An ongoing programme that delivers enhancements to systems and services—such as accessibility updates to SETS - to improve performance and user experience. |

| Declaration rates |

Annex C: Revenue Scotland People Survey - Equality and diversity

The Revenue Scotland People Survey asks if staff were discriminated against at work in the past 12 months and on what grounds. Due to small numbers, the detailed breakdown of discrimination responses has been suppressed to protect anonymity. The data is suppressed if less than 5% colleagues report experiencing discrimination.

Annex B: Gender pay gap

The gender pay gap is calculated as the difference between average hourly earnings (excluding overtime) of men and women as a proportion of average hourly earnings (excluding overtime) of men’s earnings. A positive pay gap means that men earn more than women on average, and a negative pay gap means that women earn more than men.

Annex A: Employee diversity data

The following charts show the composition of the Revenue Scotland staff body, broken down according to their protected characteristics. Data on Revenue Scotland staff is given for each of the previous three years.

The composition of Revenue Scotland staff is compared to data on Scotland's working age population. Comparator data on age and gender is taken from the National Records of Scotland’s 2024 mid-year population estimates for all people aged 16-65.

Consultation now live on modernising communications from Revenue Scotland

Scottish Government has today announced a consultation on modernising Revenue Scotland’s tax administration framework, specifically relating to communications from Revenue Scotland to taxpayers. You can view this consultation online here:

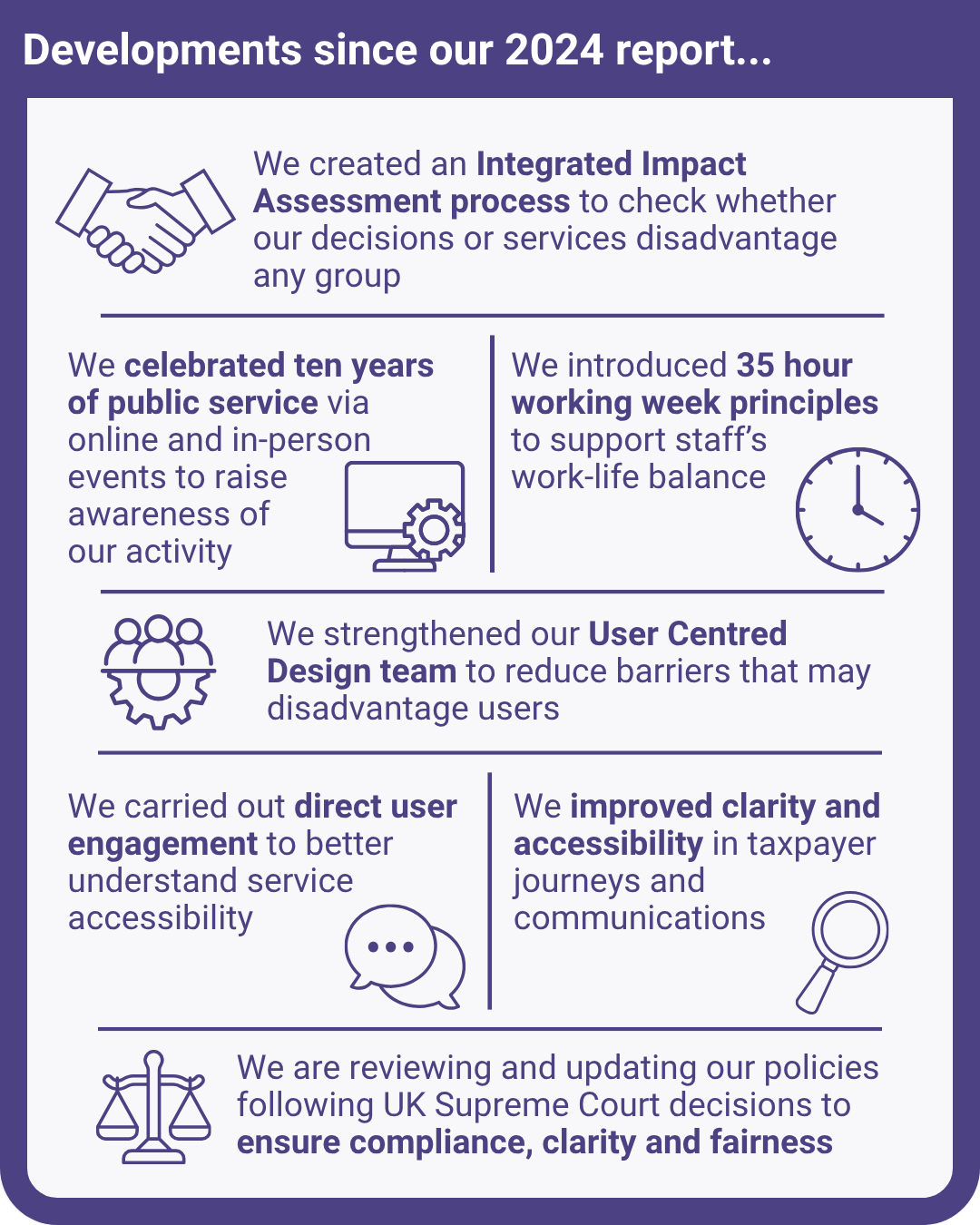

Developments since the Equalities Mainstreaming Report 2024

- We created an Integrated Impact Assessment process to check whether our decisions or services disadvantage any group

Gender pay gap

We provide at Annex B information regarding our gender pay gap and distribution between pay grades.

Employee diversity data

We provide at Annex A diversity data on our employees. Employee data remains an area of challenge for us, despite being a growing organisation of 108 employees (March 2026). Much of the data we have on our staff is subject to suppression, as shown in Annex A, and results can be skewed by missing or out-of-date information. The data should be interpreted in that light.

Progress against the 2024-2028 equality outcomes

We are pleased to report progress in relation to the outcomes and our action plan as follows.

Equality outcome 1

Revenue Scotland will actively promote equality, diversity and inclusion in designing and delivering our services.

Equality outcomes 2024-28

We publish our equality outcomes every four years and report on progress every two years.